We’re still in the early days of Blockchain as a technology, and so we’re yet to see the full impact that it will have on the world that we live in. Still, it’s already showing potential across a range of industries and started to enter the public consciousness, so the real question is what will happen when Blockchain technology starts to mature.

Right now, speculating on the future of Blockchain is like trying to predict the future of the World Wide Web in 1990. It’s just too early to say for sure, but we can at least be reasonably certain that it’s going to continue to grow as more and more uses cases are found for the exciting new technology. In the meantime, all we can do is watch and learn. [2]

In a new era of Europe’s General Data Protection Regulation (and other similar online data privacy legislation on the way), Blockchain is poised to take its place at center stage in today’s economy. It’s likely that this change will be top-down: People won’t be demanding Blockchain, so businesses will have to lead the charge in transitioning to this system. [3]

Blockchain will face many changes and obstacles but still provides many promising applications; the following list discusses both challenges and applications of Blockchain technology in 2019 and beyond:

A Reality check for Blockchain

Blockchain is suffering the same type of overhype that virtual reality is. For years, people in various sectors have been hearing about Blockchain. It’s been portrayed as a true game changer. The problem is that so many people still aren’t seeing real world benefits. To them, like virtual reality, it remains a nifty technology without a practical application they can really wrap their heads around.

In 2018, we saw an increase in funding for Blockchain startups. However, like any new technology, Blockchain is still immature in its implementation; as a result, many Blockchain startups are expected to be just a waste of time and money. False starts in Blockchain deployment will lead organizations to failed innovations, rash decisions, and even complete refusal of this innovative technology.

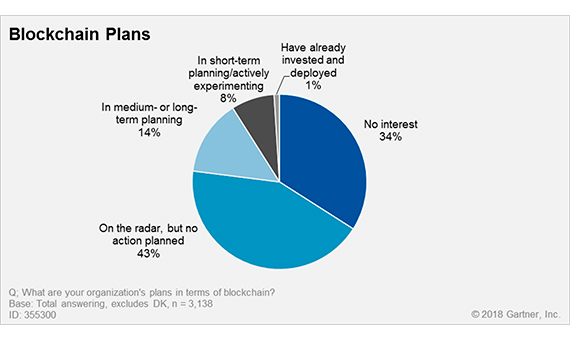

Undoubtedly, Blockchain technology in the future will affect every aspect of businesses, but this is a gradual process that requires time and patience. Gartner predicts that most traditional businesses will keep an eye on Blockchain technology, but won’t plan any actions, waiting for more examples of the best applications of Blockchain technology.

The reason for this is that traditional enterprises require more transformation for Blockchain deployment than newly-appeared businesses. According to Gartner, only 10% of traditional companies will achieve any radical transformation with Blockchain technologies by 2023. [4]

This isn’t to say that Blockchain doesn’t have amazing potential. It certainly does prove that the gap between Blockchain hype and application is a problem. If businesses stop exploring its potential, it won’t matter how useful the technology is. But this may be changing as well. [1]

The ‘Emerging Disruptor’ startups fueled by Blockchain

The Blockchain ‘emerging disruptor’ companies are fast growth startups that have found themselves in the position to be able to disrupt other businesses in their sector. They often have the benefit of being well-funded, and headed by executives who are experienced and well-connected in their industries.

These are the businesses that are often able to apply Blockchain technologies in ways that are truly a part of their business model, as opposed to supplementing it. Competing with big names like Amazon, Google, Facebook, Apple and Microsoft. [1]

For example Blockchain could be useful for content streaming companies like Netflix because it could be used to store data more securely and to pave the way for interoperability. If nothing else, it could provide something resembling an API, allowing third-parties to read and write data to the Blockchain.

But there could be a more practical use for Blockchain in the streaming industry and in other industries which require large amounts of processing power. In the same way that mining for bitcoin just taps into dormant computing power from across a network of machines, streaming companies could witness huge decreases in their operating costs by spreading the load across unused machines via the Blockchain. [2]

Blockchain and Cybersecurity

The global figure for cyber breaches had been put at around $200 billion annually [8]. Because Blockchain was created as a means to ensure the security of transactions, it shouldn’t come as a big surprise that this is the niche where much of the innovation still occurs. Blockchain is playing a huge role in cybersecurity especially. [1]

With the growing prevalence of data breaches and the massively interconnected world we live in, new ways to verify identity and protect privacy will be game changers. Blockchain is a natural for this role because the whole point of it is to provide robust, incorruptible — yet encrypted — recordkeeping that anyone can easily verify.

An example for such application; Blockchain can be used for shopping security, whether online or in person. Blockchain in this space can create a “universal shopper profile” that is undergirded by Blockchain. Unlike most systems these days, in which your purchase histories are stored and carefully scrutinized and shared by big names such as Google, Blockchain restricts the information collection and sharing to only those entities that you (the consumer) grant it to share, and give consumers incentive to see ads by tokenizing the process and give rewards. [3]

For a Blockchain system to be penetrated, the attacker must intrude into every system on the network to manipulate the data that is stored on the network. The number of systems stored on every network can be in millions. Since domain editing rights are only given to those who require them, the hacker won’t get the right to edit and manipulate the data even after hacking a million of systems. Since such manipulation of data on the network has never taken place on the Blockchain, it is not an easy task for any attacker.

While we store our data on a Blockchain system, the threat of a possible hack gets eliminated. Every time our data is stored or inserted into Blockchain ledgers, a new block is created. This block further stores a key that is cryptographically created. This key becomes the unlocking key for the next record that is to be stored onto the ledger. In this manner, the data is extremely secure.

Furthermore, the hashing feature of Blockchain technology is one of its underlying qualities that make it such a prominent technology. Using cryptography and the hashing algorithm, Blockchain technology converts the data stored in our ledgers. This hash encrypts the data and stores it in such a language that the data can only be decrypted using keys stored in the systems. Other than cybersecurity, Blockchain has many applications in several fields that help in maintaining and securing data. The fields where this technology is already showing its ability are finance, supply chain management, and Blockchain-enabled smart contracts. [8]

Internet of Things (IoT) meets Blockchain

It’s no secret that the internet of things is coming to connect our devices and to make it easier than ever for us to create and store data about ourselves. This applies to everything from wearable devices to home hubs, connected fridges and any other type of internet-connected device that you can imagine.

But all of these internet-connected devices will need some sort of security system that ties them together and that makes their data secure. That could be where the Blockchain comes in, but only if different manufacturers can agree to come together and agree on the specifications of the Blockchain that’s required. [2]

The International Data Corporation (IDC) reports that many IoT companies are considering the implementation of Blockchain technology in their solutions. Therefore, IDC expects that nearly 20 percent of IoT deployments will enable Blockchain services by 2019.

The reason for this is that Blockchain technology can provide a secure and scalable framework for communication between IoT devices. While modern security protocols already appeared to be vulnerable when implemented to IoT devices, Blockchain has already approved its high resistance to cyber-attacks. [4]

Besides, Blockchain will allow smart devices to make automated micro-transactions. Due to its distributed nature, Blockchain will conduct transactions faster and cheaper. To enable transferring money or data, IoT devices will leverage smart contracts which will be considered as the agreement between the two parties. [4]

Since the beginning of 2018, analysts have been predicting that IoT DApps might just become the next key development in Blockchain application development. By 2019, 20% of all IoT deployments are predicted to have at least basic levels of Blockchain services enabled.

IoT security flaws generally revolve around three major events: authentication, connection, and tractions.Thanks to these vulnerabilities, already hackers have managed to take control of implanted cardiac devices, disable cars remotely, and launch the largest DDos attack to date.

Given that security is one of the main challenges of IoT, as well as, data integrity, it goes without saying that Blockchain could potentially revolutionize this sector. Blockchain technology makes it possible to stabilize complex IoT systems. It also eliminates the risk of single points of failure for an IoT network as a result of malicious attacks. [6]

Increased use of smart contracts

Smart contracts are one of the most interesting aspects of Blockchain technology because they have the potential to bypass third parties and to create airtight agreements that must be honored. This has plenty of practical applications in all sorts of industries, from finance and real estate to logistics and recruitment. Any industry that relies on agreements to function can get a lot out of smart contracts.

The idea behind these contracts is that they offer increased transparency and security while simultaneously speeding up the whole process. Contracts could be signed and verified in real-time in a secure environment, and that can make all of the difference when it comes to getting things done and reacting quickly to changes in the market. [2]

You should also keep in mind that smart contracts are decentralized and aren’t regulated by any authority. But what should parties do in case of any disagreement? Participants of smart contracts usually agree to be bound by regulations, but what if a dispute appears between parties from different countries. Now, it remains to be unclear how contractual disputes should be settled. Thus, the rule of law should be enforced into smart contracts in the near future for resolving any disputes between the parties. [4]

Ahmed Banafa, Author the Books:

Secure and Smart Internet of Things (IoT) Using Blockchain and AI

Blockchain Technology and Applications

References

- [1] https://www.forbes.com/sites/andrewarnold/2018/08/13/the-6-major-Blockchain-trends-for-2018-outlined-by-deloitte/#40ac48474844

- [2] https://www.cio.com/article/3294225/Blockchain/5-top-Blockchain-trends-of-2018.html

- [3] https://www.forbes.com/sites/forbestechcouncil/2018/07/18/three-breakthroughs-that-will-disrupt-the-tech-world-in-2019/#485c59e61f87

- [4] https://aithority.com/guest-authors/Blockchain-technology-in-the-future-7-predictions-for-2020/

- [5] https://enterprisersproject.com/article/2017/12/5-Blockchain-trends-watch-2018

- [6] https://achievion.com/blog/5-trends-Blockchain-application-development-2018.html

- [7] https://hackernoon.com/latest-Blockchain-trends-to-watch-out-for-in-2018-59b2831ddfb

- [8] https://www.bbntimes.com/en/technology/second-line-of-defense-for-cybersecurity-blockchain

Comments on this publication