The relationship between banks and fintech companies has oscillated between ignoring each other, becoming tense, and even going so far as saying that the other will soon be a thing of the past. None of these solutions is best from a profit perspective, at least not in the short term. Some win-win proposition would be better for both parties and their clients.

Application Programming Interfaces (APIs) are here to bridge the gap between the old monolithic systems of traditional banks and the real-time, data-driven approach of fintech companies. This solution looks like the way to end this war and start to collaborate instead of competing.

Types of APIs

Banks are not new to using APIs, as they have been doing so internally for years to connect different platforms holding information about customers, profit, and portfolios. These types of APIs called private are not the primary focus of our talk, since they don’t offer extended opportunities to clients but are mere management tools.

The intermediate API type, or the partner API, is explicitly developed per project between a bank and a trusted partner for specific products or to reach a particular audience. These are the prototypes for the next level, but are not general enough and still under legacy architectures.

The last type is open APIs designed for non-specific partners. These are configurable, ad-hoc and considered to carry a high risk, since there is no way of regulating the relationship through a previous contract stating liabilities. The solution to this problem could be by implementing the blockchain technology which enables parties to trust each other blindly by the design of the algorithm requiring no further contracts.

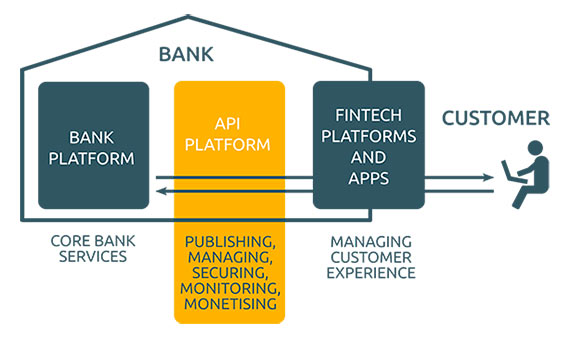

What Do APIs Do?

As their name implies, these are interfaces that allow seamless communication between different systems by offering a plug and play approach. Their role is to help the parties collaborate through an opaque channel that provides access without unveiling user credentials. The most important features of APIs are functionality, security and control, which we will detail further.

- Functionality: The primary motivation behind using APIs is the enhanced customer experience they offer through providing clients with a simplified, user-friendly interface. Also, by a collaboration between a bank and a fintech company, both can create innovative products that would have been difficult to develop individually. This speeds up the time-to-market and retains a competitive edge. The rise of new business models based on data analysis is another way APIs are bringing value to both traditional and new actors of the financial sector.

- Security: The most significant concern of banks apart from sharing their profit with various third parties is related to the safety of their clients’ personal information. Until now, this heavily regulated industry was kept safe by its closed-gate, no-transparency policy. Opening through APIs is scary and poses new challenges.

The current state of mobile app security, as described in this piece on the fintech industry, reveals that three-quarters of existing apps are not ready to pass a basic security test and 60% of apps are vulnerable at any moment.

Keeping this in mind, it is worth mentioning that APIs can secure a connection by simply defining acceptable types of requests very strictly and operating exclusively with encrypted data at all times.

- Control: Banks fear to give the keys to their customer data vault to anyone for good reasons. Through a secured and well-thought API this would no longer be a problem, as the bank could control what is shared, impose time limits to prevent brute-force attacks and monitor the network flow.

Open Borders

This is one of the most surprising effects of APIs. Until now, most banking was done domestically, with the occasional use of platforms such as PayPal for online shopping. Fintech companies helped by APIs will democratize investment and lending to offer better rates to clients, even by simply providing them with the opportunity to shop around in a browser window or by using an app. A study shows that prices for basic banking products like credit card fees and annual mortgage rates vary significantly between countries.

A Changing World

Fintech companies are forcing banks to go beyond their comfort zone, innovate and accept change as a way of staying in business. With APIs handling the translation between legacy systems and the new technologies, fintech companies can focus on providing more value to the clients instead of learning about obsolete systems.

Adopting a client-centric vision helps both banks and fintech companies fulfill their goals. For example, a bank doesn’t offer its corporate clients the ability to compare their yearly financial results with the industry average, but a fintech company can make it its value proposition and, by cooperating with the bank through an API, to help them learn more about their results. For the bank, it doesn’t make sense to create such a niche service, while the fintech’s algorithm is useless without the proper big data input.

The Legal Framework

International organizations and forums support this collaboration between banks and fintech companies since it brings added value to the client. The EU went a step further than just encouraging the initiatives and developed a directive regarding Payment services (PSD 2) which aims to remove the bank’s monopoly on their clients’ account information. The law grants the right to every customer to use third-party help to manage their finances, forcing banks to give access to these providers through APIs.

New Generations, New Expectations

The generation that boosted apps and has backed up numerous fintech startups through crowdsourcing are the Millennials, and they will be closely followed by Gen Z who have an even bigger appetite for technology and real-time data and analytics. Other highly prized features by these generations include user experience and design, integration between apps and platforms, and excellent personalization.

To please this group of customers, which is the most significant cohort so far and whose financial power is expected to rise exponentially, banks and fintech companies will need to adapt and deliver products that satisfy the expectations shaped by the retail and entertainment industries.

Comments on this publication