The importance of the Data Scientist in banking

Customers are demanding a digital transformation across all sectors, and companies have become aware of the beneficial impact on their income statement of optimizing internal processes and achieving optimal decision-making. The synergy between Data analytics, Artificial Intelligence and Big Data is the foundation for this digital transformation [1].

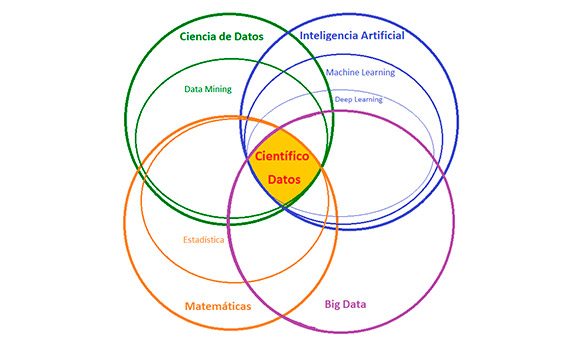

Artificial Intelligence as a whole and, more specifically with Machine Learning, makes it possible for corporate software to learn customer patterns and behaviors and to make decisions autonomously. However, to do this, human guidance is needed [2]. At the moment, Deep Learning, a branch of Machine Learning, is working to achieve fully independent software learning, with no human intervention, and consequently overcome the challenge of simulating how the human brain learns [3]. Data analytics and Artificial Intelligence techniques have been around for a long time. However, they are currently experiencing a peak in development on the basis of Big Data: it is possible to manage very large volumes of information and process it quickly and efficiently. The larger the volume of information, the more accurate the detected patterns and behaviors. For this reason, it is important to be able to rely on enormous amounts of data and to be able to process them quickly and even in real time.

The synergy between Data Analytics, Machine Learning (or Deep Learning) and Big Data enables companies to innovate in all of their structures and offer their customers fully customized and tailor-made service. Data is the oil of the 21st century, and these technologies exploit it carefully to offer bespoke services and a new perspective, which customers are already demanding [4]. The financial sector has realized that each of its customers generates enormous amounts of data each and is fully reforming itself to extract as much hidden knowledge from this information as possible. Until now, this data did not add value but now the goal is to have the customer and their data at the core of the business [5].

13 Synergies that the financial sector may leverage:

- Intelligent account: Financial institutions aim to offer their customers a new account concept by replacing the traditional “ccc” with a value-added service that allows customers to receive expense forecasts and possible short- and long-term overdraft; analyze their behavior on the basis of generated expenses; automatically categorize transactions to view them by group; compare expenses with anonymous customers with their same profile; or check product recommendations that meet their specific needs [6].

- Personalized financial products: Every customer has their own economic activity and, with data analytics, it is possible to detect patterns and behaviors [6] to offer them personalized, tailor-made financial products for a better customer experience and greater satisfaction.

- New business opportunities with the institution’s customers: In addition to the information about their customers’ economic activity, banks now can also access external information, such as data from social media or online behavior, to add to the data ecosystem surrounding each customer [7]. By analyzing external information, new business opportunities open up to the banks: if their customer uploads photos of a certain type of car and indicates their interest, the bank can generate the offer of a credit product at that exact moment, which meets the customer’s specific needs, is sent via the social network and can be materialized quickly and with “very few clicks“.

- New business opportunities for non-customers: Including the analysis of external data may generate new business opportunities, even for non-customers of the financial institution [7]. A person’s financial needs may be detected and the bank can then offer them a product for their particular circumstances and this may perhaps lead to a deal in the future.

- Risk management and fraud prevention: There are two instances of pioneering use of data analytics, machine learning and big data in banking institutions [8]: risk management and fraud prevention are two of the most important issues for banks at the moment and, for this reason, they are the first projects to have been addressed with these technologies.

- Internal recommendation engine for the physical location of branches: The financial institution must collect data about the city areas most frequently visited by its customers, what times they go there, where they shop, what type of customers they are and where there are fewer of its customers [9]; by applying analytics, institutions are able to determine the area that will generate the most benefits as a result of branch placement.

- Internal recommendation engine for the physical location of ATMs: As above, the bank must analyze the city’s areas where its customers most spend [9], how they do it and the city’s areas where its customers use ATMs from a different financial institution.

- Recommendation engine about how much money to add to ATMs on weekends and holidays: Based on the calendar of the ATM’s location, the weather conditions and the city’s events and their location, it is possible to make an accurate calculation of the right amount to add to ATMs [9]. In this way, banks avoid blocking a lot of cash in the ATM as well as service disruption because of lack of cash.

- Predicting when a customer will leave the institution: By analyzing a customer’s account activity and combining this information with internal data from other channels (branch or online) as well as external data (social media), it is possible to determine whether the customer will leave the bank. If no account activity is registered for a while, the customer does not visit the website or go to the branch, and they follow other bank(s) on social media, it is possible to predict when the customer will leave the bank [10]. When this situation is detected, it is important to be able to recommend products or improvements to keep the customer (what they have subscribed, their activity and what we can offer). It is always more economical to keep an existing customer than to attract a new one.

- Frequently used ATM operations: When they use an ATM, many of the bank’s customers complete the same operation. The goal is to determine their pattern and behavior and offer this operation directly, without questions or browsing [10]. For example, a customer that normally chooses the same operation will only have to press the button for frequently used operation when they insert their card in the machine, and the ATM will dispense 50 euros with no receipt. As a result, the customer takes a lot less time to complete the operation and there is greater customer satisfaction.

In the current financial context, with fintechs as new competitors and major online companies looking toward the financial market, traditional banks must optimize their processes and resources. To this end, they must analyze their data appropriately./ Image: CC0 Public Domain

- Analyze and determine the best means of communication with the customer: Customers demand that their bank contact them via the new channels, which they use as default: social media, email or instant messaging [11]. The financial institutions must analyze and determine the priority channel for the customer, the channel where they feel the most comfortable receiving notifications, and send them through this means. The financial institutions must abandon the traditional policy of sending notifications to channels that are not used by the customer and, as such, result in unnecessary expenses.

- New business channels to monetize aggregate and anonymous data: Customer data is the most important asset of financial institutions. However, this aggregate and anonymized information may be of great value to another bank or company to exploit [11]. For example, banks may be able to leverage a major business opportunity by selling anonymized data about frequent supply-related expenses among a certain population profile so that the sector’s companies are able to design attractive offers.

- Optimization of the institution’s processes and resources: By gathering data about the institution’s processes and resources and then analyzing it, it is possible to discover hitherto unknown patterns and behaviors to maximize benefits while incurring fewer expenses [11].

Bibliography:

- Sasa Baskarada, Andy Koronios: Unicorn data scientist: the rarest of breeds. Program 51(1): 65-74 (2017)

- Yi Yin, Anneke Zuiderwijk: Scientists. Fundamental Requirements to Deal with their Research Data in the Big Data Era. ERCIM News 2017(109) (2017)

- Frédéric Chazal, Bertrand Michel: An introduction to Topological Data Analysis: fundamental and practical aspects for data scientists. CoRR abs/1710.04019 (2017)

- Beiji Zou, Qilong Han, Guanglu Sun, Weipeng Jing, Xiaoning Peng, Zeguang Lu: Data Science – Third International Conference of Pioneering Computer Scientists, Engineers and Educators, ICPCSEE 2017, Changsha, China, September 22-24, 2017, Proceedings, Part II. Communications in Computer and Information Science 728, Springer 2017, ISBN 978-981-10-6387-9

- Carlos Costa, Maribel Yasmina Santos: A Conceptual Model for the Professional Profile of a Data Scientist. WorldCIST (2) 2017: 453-463

- Wardah Zainal Abidin, Nur Amie Ismail, Nurazean Maarop, Rose Alinda Alias: Skills Sets Towards Becoming Effective Data Scientists. KMO 2017: 97-106

- Roy Laurens, Cliff C. Zou: Using Credit/Debit Card Dynamic Soft Descriptor as Fraud Prevention System for Merchant. GLOBECOM 2016: 1-7

- David L. Olson, Desheng Wu: Predictive Data Mining Models. Computational Risk Management, Springer 2017, ISBN 978-981-10-2542-6, pp. 1-97

- Prabha Dhandayudam, Ilango Krishnamurthi: A Rough Set Approach for Customer Segmentation. Data Science Journal 13: 1-11 (2014)

- Isaac A. Jones, Kyoung-Yun Kim: Systematic Service Product Requirement Analysis with Online Customer Review Data. J. Integrated Design & Process Science 19(2): 25-48 (2015)

- Jorge López Lázaro, Álvaro Barbero Jiménez, Akiko Takeda: Improving cash logistics in bank branches by coupling machine learning and robust optimization. Expert Syst. Appl. 92: 236-255 (2018)

Javier Porras Castaño

References

- BBVA Data & Analytics: el reto de transformar los datos en valor para nuestros clientes (BBVA Data & Analytics: the challenge of transforming data into value for our customers) (click here)

- Synergic Partners: How is value extracted from Data? (click here)

- Telos (Telefónica): Hacia un nuevo modelo económico viable basado en el conocimiento (Toward a new viable economic model based on knowledge) (click here)

- 5 días: Del ‘big data’ a la empresa inteligente (From big data to the smart company) (click here)

- KDnuggets: Machine Learning as a Service: Amazon, Microsoft Azure, Google Cloud AI (click here)

- BBVA: Four interesting ideas that harness big data (click here)

- PiperLab: Big Data y los sistemas de recomendación (Big Data and the recommendation systems) (click here)

- Futurizable: Mezcla y vencerás (Mix it up to win) (click here)

Comments on this publication