We are undergoing an era of social and political change that is, at the same time, the cause and effect of a state of perplexity, uncertainty and insecurity among citizens. At its foundations are a fear of the future of the economy and employment in the context of rapid technological change and progress. This article argues that the technological revolution will produce, in the medium term, more wellbeing, growth and employment, but only after a transition period that could be difficult for many. Appropriate economic policies would help to speed this transition and minimize its costs. Among these policies must be included the promotion of a digital transformation of the financial system that contributes to greater and more inclusive growth.

Change and Perplexity

In this last decade, we have witnessed phenomena that (especially when considered in retrospect) were probably not unforeseeable, but that systematically catch even the most expert political, economic and social agents off-guard.

After eighty years in which the possibility of another Great Depression was considered unthinkable, we have suffered an intense economic and financial crisis. Concurrently, but not independently, we are witnessing profound changes in political, economic and social models: long held beliefs and assumptions are being questioned; institutions that have anchored domestic and supranational policies for many years are severely weakened.

In the geopolitical area, the regime after the end of the Cold War, in which the United States emerged as the only superpower, guarantor of an increasingly open and interconnected world, consolidating a global order of ever more integrated democracies and market economies, has given way to a much more uncertain world. Now there is no longer a clear hegemonic power. Not only because the influence of the United States in the global economy is weakening, but because other areas, especially Asia, are growing more quickly. It is also because the United States, which during Obama’s presidency already reduced its involvement in foreign conflicts, after the election of President Trump, is appearing to renounce its role as a global promoter of democracy, the rule of law, free trade and human rights to adopt a more unilateral view and use its economic and military power (the latter being clearly hegemonic) only in defense of the interests of the United States, in a much more restrictive way.

This, of course, weakens the United States’ closest, unconditional allies: Western Europe, Japan, etc., and leaves Russia or China more room to expand their political and economic influence: firstly in their closer hinterlands, and from there, to the rest of the world. Other smaller regional powers are also gaining the ability to influence their immediate surrounding areas, increasing global instability.

At the same time, supranational economic and/or political cooperation projects and the free trade agreements are losing impetus in different regions (Asia/ America, America/Europe…). Even the European integration project, that has had seen unprecedented success for decades, now faces Brexit, deep disagreements with several members in Central and Eastern Europe, and a growing disaffection of Europeans with the common project.

At the root of these geopolitical shifts we can observe changes in nations, societies and citizens themselves; we see, around the world, the growth of populist political parties, as well as a downward trend in people’s participation and trust in politics, institutions, elections, and the liberal democratic system in general. In return, ‘state authoritarianism’ and what is sometimes called ‘direct’ democracy (that is, the formulation of political proposals in which there is no institutional intermediation, supported by public opinion and that supposedly represent the will of the people, and the making of decisions based on referendums) develop.

Political rhetoric and its narratives are also changing in the case of politicians, the media or social media, with an increase in polarization and a growing tendency towards the ‘framing’ of the news or deliberate ways of disinformation, such as the use of ‘fake news’.

The result of all this is a less transparent political debate focused on solving problems in the short term, one much more oriented towards confrontation, the creation of enemies and the ‘othering’ of those who think differently, rather than the search for common ground.

In this setting, citizens feel ‘attacked’, insecure and pessimistic, and tend to support drastic solutions to their problems, and ‘defend themselves’ taking on extreme identities (nationalistic, religious or other kinds) that exclude any that are perceived as different, and therefore dangerous.

In social terms, this results in a loss of cohesion, especially between different ethnic and religious groups, and growing integration problems, with increased restrictions for different groups, but particularly in immigrant’s access to housing, citizenship, public services, the social safety net, etc.

We are living in an age that Darrell West (2016) calls an era of “mega-change”, in which social, economic and political models are no longer fixed, and this causes insecurity and fear: fear of others, fear of the future. This feeling may resemble what the sociologist Zygmunt Bauman (1998) called Unsicherheit: a complex combination of uncertainty, insecurity and vulnerability that he blamed on the economic, social and cultural consequences of globalisation and their complex adaptation in more limited contexts: national, regional or local. Similarly, before the economic and financial crisis, many economists like Mary Kaldor (2004), thought that political phenomena such as the boom of the ‘new nationalisms’ were an answer to globalisation.

What causes more concern regarding the technological revolution is its impact on the future of employment

Today, most researchers attribute these phenomena to a more complex combination of factors: to the effects (perceived or feared) of globalisation we must add those linked to the technological revolution. These effects frequently get mixed up or are identified with those of economic crisis and the austerity policies that have been imposed in many countries.

Years before, the predominant view regarding globalisation was that, ultimately, the increase in international trade and growing interdependence would promote greater global growth and consolidate democratic political systems worldwide, supporting stability and welfare at a global level. Today, these benefits only provoke more controversies: the loss of jobs (moving from developed countries to emerging nations with lower labor costs) is feared, as well as costs of all kinds —including social costs and an increase in the risk of terrorist acts— associated with migration flows.

Technological change speeds or multiplies the effects of globalization, and improvements in telecommunications, connectivity, the internet, etc. encourage economic, political and cultural globalisation. Globalized markets are the natural habitat of the technological revolution, where it can develop its potentialities.

But, beyond all this, these technological advances also harbor their own complications; they improve communication and the access to knowledge, productivity and efficiency, but they are also tools for political destabilization, crime and terrorism, because they facilitate the planning and financing of these acts. And they also create new targets for these activities: cyberattacks are directed precisely towards the enormous data volumes and the infrastructures that store, protect and transmit them, which are essential for the smooth running of the global economy and society.

Globalisation and Technology: Fears and Facts

Periods of both globalisation and great technological acceleration, have been recurrent throughout the history of humanity, and these have both normally overlapped: technological advances encourage the search for new fields where they can be applied with an advantage over the more outdated local technologies.

In this manner, the intense phase of globalization that took place immediately before this current one occurred in the latter decades of the 19th century and the first few years of the 20th century, and was driven by steam, electricity and the internal combustion engine, telegraphy and the telephone. It was a period of accelerated growth, only interrupted by World War I. This was why, after the war’s end, Keynes (1919) proposed returning to globalisation in order to relaunch growth and consolidate peace.

However, the interwar period was a time of regression for globalisation, marked by the Great Depression of 1929, and the protectionist and nationalistic reactions caused by it; however after World War II, the globalisation process restarted again with great dynamism (continuing, to a great extent, Keynes’s ideas), and this also coincided with the information revolution, that started in the 1950s and which has had seen exponential growth since then.

The second half of the 20th century and the first few years of the 21st century have seen unprecedented global expansion. The increase in productivity has made it possible to support rapid growth of the global population from less than 2.5 billion in 1945 to 7.5 billion at present. And all this with unparalleled improvement in living conditions.

According to the methodology of the World Bank, which counts the number of people that live on less than USD 1.90 per day – in 1945, more than two thirds of the world population was under this threshold: that is more than 1.6 billion people who lived in conditions of extreme poverty. In 2015, extreme poverty affected less than 700 million people (less than 10% of the world population).

This encouraging trend has increased in the last few decades. The proportion of those in extreme poverty with respect to the global population had been decreasing, although slowly, since the beginning of the 19th century, but its absolute number still grew until the 1970s. Since then, not only the proportion, but the number of people living in extreme poverty has been falling at a quicker pace since the 1990s. In 1990, those in extreme poverty accounted for 35% of the world population (some 1.5 billion people). Today, the total number has dropped to less than half of that figure, and the percentage that they represent with respect to the total population has fallen to a fourth.

Globalisation and technological advance have been the main driving force behind this progress. And recently another not entirely independent factor has also played a significant role: the strengthening of institutions in many emerging nations, with the consolidation of more stable and reliable political, legal and economic structures; the spread of the free market and the principle of the rule of law; and the improvement of legal guarantees.

As a result, emerging countries, especially in Asia, have undergone an unprecedented leap in their development, leading and driving world growth.

The growth in developed countries from the end of World War II to the great depression of 2008 has been lower than that in the emerging countries, but nevertheless extraordinary in historical terms.

In countries such as the United States and the United Kingdom, that are very technologically advanced, and have been the principal actors in the current wave of globalisation, GDP per capita has multiplied by 7.5 (in the United States) and by 5.7 (in the United Kingdom) since the beginning of the 20th century. At the same time, standard working hours have dropped from 55-60 per week to some 40 per week currently.

That is to say, globalisation and the technological progress have entailed dynamic increases in production, income and employment, with clear improvements in working conditions (Doménech et al., 2017). Other contemporary analysis, which compared economies with varying degrees of technological advance and digitalization (see Gregory et al., 2016) did not show that higher automation implies higher unemployment rates.

Undoubtedly though, there are still hundreds of millions of people that live in extreme poverty in the world, and billions of people whose living conditions are very unsatisfactory. A good number of countries, especially in Africa, have been left out of this wave of prosperity; but overall, the course of the global economy in the last decade does not warrant the growing insecurity, frustration and pessimism seen, particularly in developed countries.

To explain this, we must resort to an extremely complex combination of truths and fears, the fears being partly generated by the pessimistic extrapolation towards the future of some of these truths.

Undoubtedly, a key factor has been the global crisis, and its consequences such as the increase in unemployment, the damage inflicted on public accounts and austerity policies. The adjustments to social policies have had an especially significant impact on the population of developed countries, which is more protected and ageing rapidly. The doubts surrounding the sustainability of the welfare state, which already came to surface in previous decades and that instigated liberal-style reforms have become exacerbated after the crisis.

And the insecurity caused by this has worsened due to a combination of other factors: on one hand, immigration, which is certainly necessary (in fact, it is indispensable) for the sustainability of growth, public accounts and social protection systems. However immigrants have frequently been considered a cheap workforce that competes ‘unfairly’ against locals for jobs, keeping wages low, overloading social services and increasing their cost. And, on the other hand, the accelerated eastwards shift of the global economy, towards the large emerging countries that have been growing more quickly in the last few years.

Twenty-five years ago, the developed economies represented, approximately, 60% of the global GDP in terms of purchasing power parity (PPP); and the emerging economies the remaining 40%. Today, the proportions are the reverse: the emerging economies represent a little more than 60% of the global GDP, and the developed hardly reach 40%. In terms of the PPP, the Chinese economy is now larger than that of the United Sates. Even when assessed using market exchange rates, the emergent economies represent almost 45% of world GDP, and now, taken together China (14%) and India (6%) almost reach that of the United States (22%).

According to all predictions, this process will continue: until 2050, when the average annual growth of emerging countries will approximately double that of developed countries. China will overtake the United States as the largest world economy around 2030, and India will achieve that in around 2050. By then, six of the seven largest world economies will belong to emergent countries: Indonesia, Brazil and Mexico will overtake Germany and Japan, and Turkey will overtake Italy. The whole of Europe will represent less than 10% of global GDP.

This process denotes a partial return to the positions existing before the Industrial Revolution, which powered the West’s economic growth and political hegemony from the 19th century onward. By the end of the 18th century, Asia represented 80% of the world economy: China and India, on their own, represented more than 65%, whilst Europe did not reach 10% (Marks, 2002). In 1950, Western Europe and the United States represented more than 50% of the global GDP, and China 5%.

This swift loss of prominence of the developed countries in the global economy has reduced their political influence, and has affected their collective psychology, contributing to the sensation of decline and greater pessimism. But, surely, the fear of the effects of globalisation and the technological change on labor markets is even more significant.

As we have already highlighted that there is no evidence of negative impacts on aggregate income and employment. Nevertheless, there have been very relevant changes in the composition of employment and wages.

Globalisation has particularly affected the manufacturing sectors, which have to a large extent been moved to emerging countries, with lower labor costs. As for automation and digitalization, they have made routine and repetitive jobs redundant, and are mainly concentrated in the same sectors.

Conversely, jobs in the service sector, many of them being low-skilled with low wages (and for which most immigrants also compete), are more difficult to automate (Autor and Salomons, 2017), and the very high-skilled jobs, that are more abstract and less routine, have both increased. On the other hand, labor market instability and higher job rotation has generated a growing proportion of part-time, temporary or self-employed jobs, and this has been dubbed the ‘Gig Economy’.

This polarization of the labor market has had very significant effects on the allocation of product and income, in detriment to the share of wages in GDP.

The weakness of the rise in wages in developed countries has been one of the more clearly substantiated effects of globalisation and technological progress. According to many authors, the second factor would have been the most predominant: see, for instance, the excellent contribution by Qureshi to this book (Qureshi, 2017).

According to the OECD, the real average income of families in the United States, Germany, Japan, Italy and France has grown by less than 1% per year from the mid-1980s to 2008. This data contrasts with the previous decades that followed World War II, and the situation has worsened, in general terms, since the global financial crisis. In 2014, the real income of two thirds of families in the developed economies was below that of 2005 (National Intelligence Council, 2017).

Globalisation has particularly affected the manufacturing sectors, which have a large extent been moved to emerging countries, with lower labor costs.

Lastly, the significant increases in productivity and economies of scale and network produced in the most digitalized sectors (“winner takes it all’) have given rise to a great accumulation of wealth and income in small, concentrated sectors of the population.

All this has very substantial implications on global income distribution, which are summarized very well in Branco Milanovic’s (2016) well-known ‘Elephant Chart’.

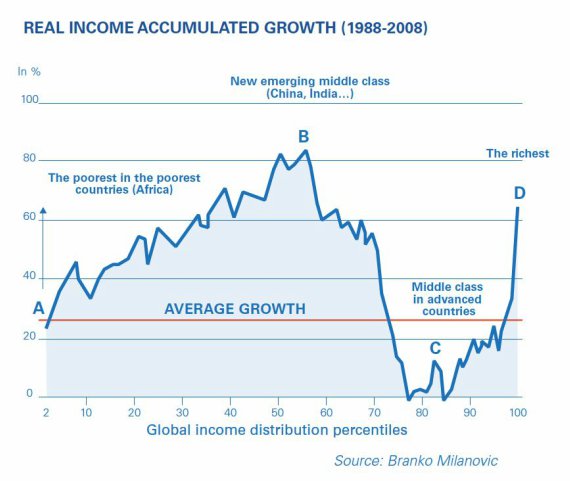

In this chart, which has now become widely known, we see the real income accumulated growth of the population of twenty (developed and emerging) countries arranged according to income percentiles between 1988-2008.

The average of the real increase in income is 25%, but the curves that give the chart its elephant shape, tell us that the distribution was very uneven: those that came off better in the two decades were the ones that are, on the one hand, between percentiles 10 and 70, and on the other hand the ones above percentile 95 (especially percentile 99). However, the lowest percentiles (below 10%) and the higher ones (between percentiles 70 and 90) have had much lower increases in real income (close to 0 for certain segments).

This is to say, the winners in these two decades of globalisation and technological progress are the wealthy, both in developed and emergent countries, working women and the new middle classes, mainly in India and China. Conversely, the losers have been, on the one hand, mainly the poorest among the poor, but not only in sub-Saharan Africa, and the lower and middle classes in developed countries and in many of the nations of the old communist bloc.

In conclusion, the global economy has had a very favorable evolution since the mid-20th century. Nevertheless, the depressing effect of the financial crisis and of the subsequent austerity policies, wage stagnation and the increase in inequality in developed countries and, also, the greater global geopolitical instability, that has triggered flows of immigration, have augmented a body of opinion that is against globalisation, and which is very distrustful about the effects of the technological revolution, especially regarding employment. All this has meant, in the political scenario, a consolidation of defensive, nationalistic and protectionist trends.

The Technological Opportunity

Today’s accelerated technological change makes it even more difficult to predict the future of the global economy. Undoubtedly, for many this makes it all the more encouraging, but for others it only adds more risk to a situation already full of threats.

The ‘current technological revolution could change our economy, our society, our everyday life… to a magnitude even greater than the Neolithic Revolution or the first Industrial Revolution, and at a much higher speed’. Brynjolfsson and McAfee (2014) have called the period that is now underway ‘the Second Machine Age’, and there is a basic difference with respect to the first: that was based on the steam engine to get over the physical limits of men and animals. The current revolution relies on the digital technologies to overcome the limits of human intellectual abilities. The rapid progress of artificial intelligence, robotics or biosciences will force us, in the not very distant future, to undergo a far-reaching reassessment of the bases of our economy, society and culture, our ethical principles and even our basic ontological foundations.

To all this uncertainty, we must add that, in the last few years, global economic growth and productivity have experienced lower performance than in previous decades, in contradiction to the historical evidence that periods of technological acceleration cause substantial increases in productivity and growth.

This contradiction has provoked intense debate among economists, and I have referred to it in more detail in a previous book of this same series (González, 2016). In short, the controversy appears to be that the ‘techno-pessimists’, think that digitalization is having a lower impact on productivity than other innovations of the past (Gordon, 2016) and/or that its positive effect is counteracted by the demographic decline in developed countries and/or by the increase in inequality, that persistently depresses aggregate demand (Piketty, 2013; Stiglitz, 2015).

On the other hand, we find the ‘techno-optimists’, who are those that think that there is problem of under measuring products, because improvements in quality and their benefits are not calculated correctly, or because they are increasingly concentrated in services and intangible assets, that are much more difficult to assess (Feldstein, 2017); or, in other cases, that we are in a transition stage that is still greatly affected by the consequences of the crisis. The global economy may still be going through a much-needed period of deleverage and correction of the weaknesses of the global banking system, which depresses consumption and investments along with the provision of public services. If this is the case, this stage would be followed by another one of much quicker growth encouraged by the technological progress.

In fact, historical experience shows that new technologies, and especially the most disruptive ones, need some time until the moment comes when their price and level of adoption allow their widespread use, when they also combine with other technologies. And from that point on, they have an increasingly stronger impact on productivity and living conditions. Brynjolfsson and McAfee (2014) think that we are reaching that turning point, which would equate to the start of what Klaus Schwab (2016) calls ‘the Fourth Industrial Revolution’.

If this were so, we could be entering a period of high growth and improved wellbeing driven by a combination of different technologies, including computing, increasingly complex, interconnected networks, artificial intelligence and cybernetics, biotechnologies and, probably, others that we do not even know of yet.

The positive effects of technological change have always appeared after a transitional process, with winners and losers.

History shows that in the same way that technological progress brings about growth and wealth, it also creates jobs. More jobs, very different from any previous, more productive, that improve people’s lives—in spite of growing inequality— (Mokyr, 2014; Autor, 2015). This is also what we have seen in the last few decades.

Despite all this, some authors have pointed out that this time it could be different, even if growth accelerates. In the first place because the advances in robotics and artificial intelligence will replace not only the people that carry out routine jobs, but also those with increasingly higher qualifications who carry out non-routine jobs. Secondly, because technology offers people the possibility of doing more things for themselves, reducing the need for jobs in the service sector. And lastly, because swift technological progress would force people to retrain themselves and to change jobs more frequently as more and more tasks are susceptible to automation. This higher friction (the need for more frequent adjustments in people’s skill set) would increase unemployment structurally.

Using these arguments, authors like Frey and Osborne (2013) have pointed out that up to 47% of the employment in the United Sates would be at risk of being automated. Others (Arntz et al., 2016), however, show that if we bear in mind the different tasks implied in each job, only 9% of the employment is automatable, as an average, in 21 OECD countries. The latter would, for instance, be a much lower figure than that of the jobs lost in the agricultural sector in the last few decades, which have been regained, undoubtedly, in other sectors.

In conclusion, it is impossible to foresee the magnitude and the speed at which the effects on growth, employment, equity and general welfare caused by such a vast technological revolution that is being born will show.

We can fear all kinds of dystopias, but we can also consider the technological revolution as a great opportunity to improve the welfare of citizens all around the world.

Even if, as many of us believe, progress and social welfare have always been the result of technical advances (and that this time does not have to be an exception), positive effects have always appeared after a transitional process, with winners and losers. And this Fourth Industrial Revolution poses especially complex challenges.

In any case, the results will always be better and the costs lower if the right policies are implemented: policies that do not create any resistance against technological progress, but rather promote equal opportunities; that means, making them available for all, and reducing transition costs in the short and the medium term.

There are lines of action that contribute, simultaneously, in order to reach all these goals. To attain this, we must promote research, development and innovation, as well as entrepreneurship, and encourage transparency and competitiveness in the markets, and develop the required infrastructures.

Equal opportunities requires an exceptional effort in the area of education: education focused on obtaining additional skills that do not replace those required for technological progress, that promotes continuous education and ongoing training, and which evolves along with the needs of society.

The labor market must be another important priority. Barriers to the growth of companies, investment and job creation must be eliminated; better active and passive policies against unemployment must be developed; a balance in taxation must be found so that redistribution does not damage investment; and regulation must be updated to care for the wider diversity of employment status and the needs of self-employed workers.

In spite of these policies, transition costs could still be considerable for certain segments. Due to this, it is vital to develop social protection systems that guarantee equal opportunities and provide protection for people in a very changing environment, with high employee turnover and very different kinds of jobs. These policies must be closely integrated with education and employment systems designed to reduce economic and human costs.

But this task of encouraging the adaption of our economy and our society to the technological revolution, obtaining the most from it while reducing its costs to a minimum, does not only belong to the public authorities. It is also the task of companies and people, the whole civil society. And in this scenario, the financial system and its institutions can play a very important role.

A Financial System for Inclusive Growth

There are differences in opinion regarding the direction, magnitude and speed of the impact of the technological revolution on the global economy, but there are none regarding its disruptive effect on production sectors and companies.

The first sectors that experienced disruption coming from the development of the internet and the digital economies were those with a greater informational content in their inputs or outputs: communications, media, music, many distribution sectors, etc. These industries have already transformed completely, with great improvements in efficiency and productivity, and therefore they have been able to offer consumers new and better products at a very low cost.

In most cases, these changes arrive to the market brought by new, more innovative and agile competitors. This is much better to satisfy the demands of a quickly growing wave of consumers that have developed new needs and habits, thanks, to a great extent, to the access to more and better information and to the greater connectivity permitted by intelligent mobility.

In most of the cases, these changes arrive to the market brought by new, more innovative and agile competitors. This is a much better to satisfy the demands of a quickly growing wave of consumers that have developed new needs and habits, thanks, to a great extent, to the access to more and better information and to the greater connectivity permitted by intelligent mobility.

All this forces companies to reinvent the way in which they design, produce and distribute products and services, and generates profound changes in companies and their sectors. This is already happening in industries that rely completely on material assets and on physical services to clients, such as the hotel or the transportation industries. Airbnb or Uber both show us that the technological revolution has no sectorial barriers.

Something that is demonstrating great power regarding the disruption of consolidated sectors is the development of platforms that are leveraged in exponential technologies (cloud computing, mobile connectivity, big data, artificial intelligence, blockchain, etc.) that traverse supply and demand, putting numerous suppliers and clients in touch. These innumerable interactions produce an enormous amount of data and information that allows companies in turn, to create and distribute products and services with new features that offer clients a much better experience.

Today, the five largest companies in the world in terms of market capitalization (Apple, Google, Microsoft, Amazon and Facebook) are, basically, platforms of this kind.

The banking system is an industry with an extremely large amount of information: its inputs and basic products are data, or information, and money; and the bank’s money is, ultimately, an ensemble of accounting entries, which is, information.

As a result of this, it could have been an early example of digital transformation. But even though the banking system has changed very much in the last two decades, it has not undergone changes of a magnitude similar to those in other aforementioned sectors. And this is due to several reasons: in the first place the conservatism of most of the people that have money; secondly, the strong growth and profitability of the industry in the period previous to the great crisis did not encourage radical change; and thirdly, and this is fundamental, regulation, that on one hand limited the freedom of banks to innovate and, on the other hand, protected them against the entrance of new competitors.

But all this is changing. Basically, it is the clients who are changing. A new generation of clients has grown up in a digital environment and it demands different services and new ways of gaining access to them. Banking’s traditional clients also attracted by the advantages of a new offering, and are increasingly following this trend.

Hundreds or thousands of new suppliers (mainly start-ups or, in some segments, large digital companies) are already supplying solutions to these demands. These companies do not have the costly legacy of banks, in the form of obsolete structures and systems, and can work faster, more flexibly and cheaply.

On the other hand, the banking system faces an environment of much lower growth and profitability, with very low interest rates and much more demanding regulation, stemming from the global financial crisis. All this increases the pressure and the urgency for banks to take advantage of the abilities of technology to improve their productivity radically.

Lastly, regulators already perceive, together with the risks, the ability of technology to improve the financial industry and, as a consequence, they are already modifying regulation to reinforce competition, preferably in those segments or products that have a lower impact on its stability. This has favored the entrance of new competitors in market niches such as retail payments and others.

Present technologies (not to mention those that may be developed) have enormous potential to transform the banking system. We are already witnessing great changes, but the future implications are almost unimaginable: cloud computing allows the storage and processing of an unlimited volume of data with greater agility at much lower prices. The mobile phone has already radically changed people’s lives, and has become the main contact point with banks, with increasingly larger and better functionality. Big Data analysis has innumerable applications, and it is absolutely decisive for dealing with the multitude of different financial and non-financial demands in a customized way in real time. Biometry allows for secure operations with clients, without the need of the physical presence or documents. Distributed ledger technologies (such as Blockchain) could eliminate the need for intermediaries in a great variety of transactions, changing the status quo of the banking system (as well as that of many other industries). Artificial intelligence makes it possible to automate increasingly complex cognitive tasks, and this alters the way in which clients are served and the solutions that they may be offered.

All this entails, potentially, enormous benefits for consumers and companies in terms of quality, variety, convenience and the pricing of products. And it will also allow thousands of millions of people, in the lower income strata, and to whom the conventional banking system cannot reach efficiently and profitably, to gain access to financial services, increasing their chances of prosperity and improving their lives.

In the macroeconomic sphere, this transformation of the banking system equates to a formidable structural remodeling: price cutting, the expansion of financial resources and their fine-tuning to the needs of each user will have a very positive effect on growth and reducing poverty and inequality. But the degree to which we achieve that depends, to a large extent, on the decisions that we all take, both the banks that operate in the market and the public authorities, and in this case, and principally, on financial regulators and supervisors.

The profound evaluation of financial regulation is an indispensable task, but it is also extraordinarily difficult. In the first place because the technological and competitive scenario changes constantly and will continue to do so in the future; and in the second place because digital means global, and the new regulatory framework must have a much larger degree of international homogeneity than the current one.

Basically, it is banking Clients who are changing

The challenge for authorities is to design and implement a regulatory and supervisory framework that accomplishes an appropriate balance between the improvements in efficiency and productivity, and the preservation of financial stability and consumers’ protection. And all this in a changing environment with a multitude of new suppliers provided with state-of-the-art technologies whose implications may not have been tested well enough. That is to say, to support innovation by maintaining an adequate degree of protection against the risks that it entails.

Together with this, and given the initial diversity of the organizations that participate in the market, from the closely regulated big banks to the start-ups, including the large digital companies, a balanced competitive field must be created, focused on the fact that similar products and services must receive a similar treatment, regardless of the organization that provides them. And lastly, it must have a ‘holistic’ comprehensive approach, in the sense that it must have in mind all the angles of the question: technological, legal, financial and competitive. And finally, it must be a closely coordinated framework at the supranational level, open and flexible enough to face future changes.

Regarding the participants in the market themselves, they face a very complex scenario. The sector is becoming fragmented due to the entrance, every year, of hundreds of new competitors that join the more than 20,000 banks that still exist around the world. On the other hand, the industry is becoming disaggregated as these new entrees break the banking system value chain, offering highly specialized products and services focused on very specific market niches in this value chain. Most probably this trend will reverse in the future: primarily because the banking system is a sector that already demonstrated strong overcapacity, something the aforementioned phenomena exacerbated even more. Therefore, we must expect that many banks will disappear together with many start-ups, whose mortality rate is always very high. In this way, technological change might be the factor that triggers a much-needed consolidation of the sector.

On the other hand, the users’ convenience demands much more complex and integrated solutions, and points towards the need of re-aggregating supply, and this will require the combination of different products and services offered by different suppliers.

In light of what has happened in other sectors, this re-aggregation will most likely be achieved through platforms where different suppliers will complete and will also, and very frequently, cooperate to better meet the demands of clients.

Probably, the number of these platforms will decrease, and their scope will become wider due to the huge economies of scale and network that they may generate.

A future might be foreseen in which there are a multitude of participants in the financial industry, most of them highly specialized, and that cooperate and compete in a few large platforms. Therefore, only a few of these participants will have a central role, as the ‘owners’ and ‘managers’ of these platforms. By implementing the rules, validating the transactions, and thereby controlling the information generated and the accesses to the final clients, they represent an enormous source of value.

Obviously, the competition to reach this lofty position will be very fierce, and we do not know what kind of companies will actually arrive there: particularly successful start-ups? Large digital companies? Banks that know how to adapt to this new environment? Unquestionably, very few of the present banks will accomplish it, but those who do will have to have started well in advance, a very complex and radical transformation process. This is the process that BBVA began a decade ago in search of excellence in the digital era.

And it is this competition, this search for excellence, what will take us to a much better, more efficient and productive financial system capable of designing and offering better solutions for a larger number of users (including the thousands of millions that cannot currently access the financial services) capable of encouraging growth and an increase in wellbeing that includes everybody.

Financial Inclusion:The Digital Opportunity

Nowadays there are some 3.2 billion banking customers, that is to say, people who have an account with which to make financial transactions (more than 90% in banks, but also in credit unions, postal banks, microfinancing institutions, etc.).

But more than 2 billion people (40% of the adults in the world) do not have access to any kind of ‘formal’ financial service. These people are concentrated in the areas of the world with lower incomes, but also in countries with medium or high incomes.

The rate of people excluded from financial services is even higher in the case of women and of people that live in rural areas, and even higher as we descend the scale of poverty. Also, around 200 million small and medium-sized enterprises in the world do not have access to enough credit or to no credit at all.

It is well known that entrepreneurship, and along with it, investment, economic growth and welfare, are severely damaged when savings are not directed productively, when payments become difficult and credit is scarce and expensive.

The benefits people receive from financial inclusion are extremely important: they can increase spending, resist shocks, manage their risks, invest in durable goods, health and education, and start small businesses. Due to the positive effects of the creation of small and medium-sized enterprises, individual and collective wellbeing and economic growth reach a significant level in the medium and long term. There is also strong evidence that the expansion and deepening of financial intermediation also improves the distribution of income.

Up to now, the expansion of the financial services to wider population strata met with the problem of costs. The conventional banking system was incapable of profitably offering financial products and services for small costs, frequently in distant places, at prices assumable for their clients.

Nevertheless, little by little, advances have been made. In the last few years, access to banking services has improved notably. In the last decade almost 200 million accounts have been opened each year around the world.

Many of them were opened in countries with medium and low degrees of development; and increasingly higher percentages are accounts of people in the 40% lowest income group. As a result, from 2011 to 2014, the proportion of adults in this segment with access to financial services grew from 41% to 54%.

More than 90% of these accounts were opened in financial institutions, and therefore, less than 10% were accounts in mobile phones. In conclusion, in 2014 only 3% of the poorest had an account on their cell phone, and the rest (97%) in financial institutions (Demirguc-Kunt et al., 2015).

To maintain this access to banking services, financial organizations have resorted to several strategies to lower service costs: the more penetrating use of ATMs; agreements with ‘retailers’ that provide access to low-cost and convenient service points for the user; the use of agents, normally small businesses, especially useful in remote areas; investments or association agreements with microfinance institutions; and, increasingly more, digital banking (including electronic money). Digital banking also opens up possibilities for collaboration with partners that contribute to the improvement and the reduction of the price of the supply to the clients: telecommunications companies, fintechs, governments, multilateral organizations…

All these options have been useful and will still remain so, but today, the greatest influence for encouraging financial inclusion is, without a doubt, the expansion of the digital finances supported by mobile phones.

Mobile phones are becoming omnipresent and offer increasingly more features as the networks increase their coverage. Today, some 85% of the adults in the emergent economies have a mobile phone contract, and this proportion is still growing. It has been calculated that the cost, in the emergent countries, of offering a client a digital financial account is between 10% and 20% of that of a physical account. This allows the opportunity of a profitable supply of many more products for the clients. And as more and more people and businesses use these services, economies of scale and network are being created that improve the products and make them cheaper, generate a better efficacy for the users and encourage their adoption. An example of this is the case of the mobile money M-Pesa system in Kenya, that was launched in 2007 and that now includes 70% of the adults in that country. It is certainly a restricted system, and the supply of a wider range of financial services may take more time, but payments through mobile phones are the entrance door for other products and services. And, in any case, the ‘digital’ financial inclusion process will always be quicker than the conventional alternative, which could go on for generations.

In this process, the general interests and those of the financial services suppliers converge.

A report by the McKinsey Global Institute (Manyika et al., 2016) estimates that financial inclusion could reach 1.6 billion people in a decade. Of this number, 880 million are women and this will further their emancipation and will greatly improve their families’ economic situation and welfare.

All this could increase the GDP of emerging countries by 6% by the end of this decade, and create almost 100 million additional jobs, with obvious improvements in people’s living conditions, the encouragement of businesses and improvement in the public accounts of these countries due to the increase in sales and to a better fiscal control. In turn, the suppliers of these services will be able to add up to 380 billion in revenue (CARE Accenture, 2015).

Because of this, financial inclusion is also going to become an area of competition between the more qualified financial institutions to face this challenge and also other companies: fintechs, payments providers, telecommunications companies, large retailer companies, etc. In many cases, this competition is already giving way to collaborative agreements between different kinds of companies: mainly, but not only, between banks and telecommunications companies. These agreements are being joined into by NGOs with local implementation, which improves credibility and client access, and can advise in the development of the most appropriate products and services, as well as of national or multilateral development public bodies.

This competition and collaboration process will favor the development of better products and service, at lower cost and with more convenience for users. In this way, financial inclusion will become a driver that encourages gradual access to more complex products and services, enhancing opportunities and the welfare of people, speeding up economic development and contributing to gender equality and social stability.

The greatest influence for encouraging financial inclusion is, without a doubt, the expansion of the digital finances supported by mobile phones

It is, therefore, a great opportunity that, what is more, one that does not require enormous investment or infrastructure with a long operating cycle. Mobile phone technology is the factor that is changing the rules of the game. Some 85% of the adults in emergent countries have a mobile phone, and more than 90% have access to networks whose bandwidth is increasing: 3G and 4G coverage is growing quickly.

Nevertheless, resolute and arranged action carried out by governments, companies and NGOs are needed as well.

In first place, it is important to expand mobile networks to many remote areas of these countries (generally the poorest ones). And the interoperability between communications and the payment and finance networks is crucial.

In second place, the problem regarding identification must be solved. In emergent economies, an average of 20% of the population is unregistered or has no ID. And many more do not have the documents needed for signing a contract, opening a bank account, etc. On the other hand, identification documents are not always appropriate for digital authentication. Fortunately, technology offers increasingly reliable and cheap biometric systems. And it is the job of the governments to implement universally accepted identification systems that use technological advances to control fraud (and, therefore, facilitate and make the expansion of financial services cheaper).

Governments, in collaboration with the industry and NGOs, also have, when appropriate, other tasks: foremost is to improve financial education. Another is to strengthen their country’s payment infrastructures. And lastly, to design and implement appropriate regulation that protects consumers and which, at the same time, allows suppliers to invest, compete and innovate.

All these are complex tasks, sometimes postponed in favor of others that are apparently more urgent. Nevertheless, their consequences are very positive shown by the fact that they have occupied increasingly important positions in the agendas of many emergent countries’ governments and of the multilateral organizations concerned with development. And the final objective is not far away now. The World Bank has set itself the goal of reaching universal financial inclusion in 2020. But although this goal is very ambitious, there is a very real hope of reaching it before the end of the decade.

BBVA:Transforming to Create Opportunities

BBVA is a financial group with a history dating back more than 150 years, the result of the incorporation of more than 150 banks and financial institutions of all kinds. The group is present in more than 30 countries, with an especially strong presence in Spain, Latin America, the United States and Turkey; with 71 million clients, 84,000 offices, and more than 132,000 employees around the world. It is a successful financial institution, among the most efficient and profitable in the world.

Despite this efficiency and profitably, in 2007 BBVA started a long, difficult and uncertain transformation process in order to adjust to the accelerated technological advances and the changes they are producing in the economy, society and people; changes that are unquestionably disrupting the status quo and that are going create to a completely new industry in which BBVA wants to play a leading role.

First of all, it is important to highlight that this is not only a technological, but also an organizational and, mostly, a cultural transformation. We have worked for many years on our platforms, which we have been adapting to suit the new paradigms, from the development of cloud computing, to building an open platform that allows collaboration with our developers on client technology, and the contribution of external specialists. At the same time, we have radically transformed our organization to place digital transformation at the core of all our business, to promote cultural change, and provide ourselves with the skills needed to successfully compete in the new banking industry (in González, 2016, there is a more detailed description of BBVA’s transformation process).

And lastly, we have approached the fintech ecosystem to understand, learn and incorporate new ideas and abilities. We have collaborative agreements with different state-of-the-art digital companies, and we have developed a very ambitious acquisition and investment program in very promising start-ups. Also, in 2009 we launched OpenTalent, a program for entrepreneurs that connects these start-ups with BBVA in a search for opportunities of collaboration. In this latest 2017 edition, 798 start-ups from 73 countries participated. In short, we are leveraging ourselves in the fintech system to develop a better value proposition for our clients.

Because, at the end of the day, the focus of all our efforts is the client. We want to provide them with clear, simple, transparent and fair solutions, the very best that exist. More than that, we aspire to help them to make the most appropriate financial decisions, providing them with the most suitable advice. And all this, by means of an easy, convenient customer experience that is fully attuned to their needs, completely autonomous when they prefer (‘do it yourself’) or, in other cases, through digital channels or with human interaction.

Ultimately, our transformation strategy is expressed perfectly our well-defined purpose: “To Bring the Age of Opportunity to Everyone”. At BBVA we see ourselves as facilitators of these opportunities for our clients.

In order to do that, we are creating a multitude of better products and functionalities; and we are developing new relationship models with our clients by combining all the different channels, improving them so that clients can interact with them any time they choose at their convenience.

The results of all this effort are already becoming apparent. In the few last years we have radically enhanced of our digital and multichannel offer. Our Mobile Banking app was judged to be the best in the world in 2017 by the most prestigious consultancy firm regarding these matters.

In June 2017 we already had 20 million digital clients, with an increase of 22% on the previous year. Among them, almost 15 million were mobile clients, with an increase of 42%. And this all makes for a better client experience: by the end of 2016, BBVA was already the leader in terms of our client satisfaction, as measured with the NPS (Net Promoter Score) index, in seven of the eleven countries in which we work in retail banking, and we hold the second or third place in three other countries.

Today, BBVA is at the cutting edge of the global financing system. There is still much to do; technology changes constantly and competition is increasingly fiercer. But we are contributing, through our daily work, to make the opportunities afforded by the digital era increasingly available to our clients; our objective is that people and companies may realize their hopes and dreams. This goal hopefully translates into growth and wellbeing for those in the countries where we work.

BBVA has an important presence in emerging countries; and in these countries, it is especially important to promote financial inclusion. BBVA has developed a financial inclusion model that allows us to reach people with the lowest income in these countries through alternative solutions with a lower cost than that of the conventional banking model. This strategy is based on some 50,00 orrespondent banks, businesses and institutions (chain stores, chemists or supermarkets) that act on behalf of the bank and where clients can carry out simple operations, such as deposits or withdrawals derived from the mobile banking model.

Mobile banking is the second and increasingly more relevant tool that BBVA uses for financial inclusion: it allows us to create low-cost financial solutions with non-traditional methodologies for risk evaluation and for creating an integrated client experience by combining different channels.

At the same time, BBVA has developed specific initiatives for promoting entrepreneurship among those people that have fewer opportunities. We began The Momentum Program in support of social entrepreneurship, to promote innovative social businesses (since its launch in 2011, 112 companies have participated in this comprehensive support program that includes financing, of course, but also training, strategic accompaniment and promotion).

Concurrently, BBVA has created the BBVA Microfinances Foundation, which offers vulnerable entrepreneurs personalized attention, giving them access to a complete set of financial products and services, as well as advice and training so they can improve the management of their businesses.

Since its creation, the Foundation has disbursed USD 8.4 billion for low-income entrepreneurs in Latin America. It has almost two million clients, 58% of them women, and it has a direct social impact on almost 7.5 million people.

Lastly, BBVA has an area specialized in financial inclusion within its research department that is responsible for designing and following reliable indicators, as well as analyzing improvement opportunities and facilitating in-depth discussions regarding financial inclusion.

BBVA also undertakes very important work in the area of education and the generation and dissemination of knowledge.

A very significant part of this task is concerned with financial education: in 2008, BBVA launched a Financial Education Global Plan that, since its foundation, has benefited more than 4 million people (more than 2.1 million children, 400,000 adults and more than 34,000 small and medium-sized businesses in 2016).

The BBVA Foundation is this banking group’s main tool to support knowledge: on the one hand, through research grants, and on the other hand with specific focus on the recognition and visibility of those who contribute to scientific-technological advances. The principal example of this work is the Frontiers of Knowledge Award, which are already well-known globally. Concurrently to the work of the Foundation, BBVA develops other education and knowledge diffusion programs, among which are programs concerning education in ethical values and the access to education to promote social integration and the training of children and young people. The OpenMind Project, our knowledge community, of which this book forms a part, stands out too.

To sum up, BBVA is involved in an ambitious project with which it aspires to lead the transformation of the financial industry; a transformation that must produce a financial system able to take full advantage of technological progress in order to improve opportunities for everyone and encourage more inclusive, sustainable growth, thereby improving the lives of citizens all over the world.

References

ARNTZ, M.; GREGORY, T. and ZIERAHN, U. (2016): “The Risk of Automation for Jobs in OECO Countries. A Comparative Analysis”. OECD Social, Employment and Migration Working Papers, no. 189, OECD Publishing, Paris.

AUTOR, D. H. (2015): “Why Are There Still so Many Jobs? The History and Future of Workplace Automation and Anxiety”. Journal of Economic Perspectives, vol. 29, no. 3.

AUTOR, D. H. and SALOMONS, A. (2017): “Does Productivity Growth Threaten Employment?” Paper prepared for the ECB Forum in Central Banking, Sintra, June.

BAUMAN, Z.: Globalization: The Human Consequences. Columbia University Press, New York, 1998.

BRYNJOLFSSON, E. and MCAFEE, A.: The Second Machine Age: Work, Progress, and Prosperity in a Time of Brilliant Technologies. W.W. Norton&Company, New York, 2014.

CARE ACCENTURE FINANCIAL INCLUSION REPORT (2015): “Within Reach: How Banks in Emerging Economies Can Grow Profitably by Being More Inclusive” http://www.care.org/sites/default/files/documents/Within-Reach_CARE-Accenture-2015.pdf

CHESTON, S.; CONDE, T.; BYKERE, A. and RHYNE, E. (2016): “The Business of Financial Inclusion: Insights from Banks in Emerging Markets”. IIF Center for Financial Inclusion, Washington.

DEMIRGUC-KUNT, A.; KLAPPER, L.; SINGER, D. y VAN OUDHEUSDEN, P. (2015): “The Global Findex Database 2014: Measuring Financial Inclusion around the World”. Policy Research Working Paper, no. 7255. World Bank, Washington, DC.

DOMÉNECH, R.; GARCÍA, J. R.; MONTAÑEZ, M. and NEUT, A. (2017): “El Futuro del Empleo”. BBVA Research, Madrid.

FELDSTEIN, M. (2017): “Underestimating the Real Growth of GDP, Personal Income, and Productivity”. Journal of Economic Perspectives, Spring.

FREY, C. B. and OSBORNE, M. A. (2013): “The Future of Employment: How Susceptible Are Jobs to Computerisation?”. Technological Forecasting and Social Change, vol. 114, issue C, 254-280.

GONZÁLEZ, F. (2016): “El Próximo Paso en Finanzas: la Banca Exponencial”. In El Próximo Paso: La Vida Exponencial. BBVA, Madrid, 2016.

GORDON, R. J. (2016): The Rise and Fall of American Growth: The U.S. Standard of Living since the Civil War. Princeton University Press, 2016.

GREGORY, T.; SALOMONS, A. y ZIERAHN, U. (2016): “Racing With or Against the Machine? Evidence from Europe”. ZEW Discussion Paper, no. 16-053, Mannheim.

KALDOR, M. (2004): “Nationalism and Globalisation”. Nations and Nationalism, vol. 10, 161-177.

KEYNES, J. M.: “The Economic Consequences of Peace”. Mc Millan, London, 1919.

MANYIKA, J.; LUND, S.; SINGER, M.; WHITE, O. y BERRY, C.: (2016): “Digital Finance for All: Powering Inclusive Growth in Emerging Economies”. McKinsey Global Institute.

MARKS, R. B.: The Origins of the Modern World: A Global and Environmental Narrative from the Fifteenth to the Twenty-First Century, 3rd edition. Rowman&Littlefield, Lanham, MD, 2002.

MILANOVIC, B.: Global Inequality: A New Approach for the Age of Globalization. Belknap Press of Harvard University Press, Cambridge, MA, 2016.

MOKYR, J. (2014): “Secular Stagnation?. Not in Your Life”. In Secular Stagnation: Facts, Causes, and Cures. C. Teulings and R. Baldwin, eds. CEPR Press, London, 2014.

NATIONAL INTELLIGENCE COUNCIL (2017): “Global Trends. Paradox of Progress”. NIC 2017-001. Washington.

PIKETTY, T. (2013): Capital in the Twenty-First Century. Harvard University Press, Cambridge, MA, 2013.

QURESI, Z. (2017): “Higher Tech but Growing More Slowly and Unequally: Paradoxes and Policies”. In La Era de la Perplejidad: Repensar el Mundo que Conocíamos. BBVA OpenMind, Madrid, 2017.

STIGLITZ, J.: “Rewriting the Rules of the American Economy: An Agenda for Growth and Shared Prosperity”. Roosevelt Institute, 2016.

SCHWAB, K. (2016): The Fourth Industrial Revolution: What it Means, How to Respond. World Economic Forum, Geneva.

WEST, D.: Megachange: Economic Disruption, Political Upheaval, and Social Strife in the 21st Century. Ed. The Brookings Institution, Washington DC, 2016.

Comments on this publication